rand('state',0);

randn('state',0);

n = 10;

N = 100;

Strue = sprandsym(n,0.5,0.01,1);

R = inv(full(Strue));

y_sample = sqrtm(R)*randn(n,N);

Y = cov(y_sample');

alpha = 50;

cvx_begin sdp

variable S(n,n) symmetric

maximize log_det(S) - trace(S*Y)

sum(sum(abs(S))) <= alpha

S >= 0

cvx_end

R_hat = inv(S);

S(find(S<1e-4)) = 0;

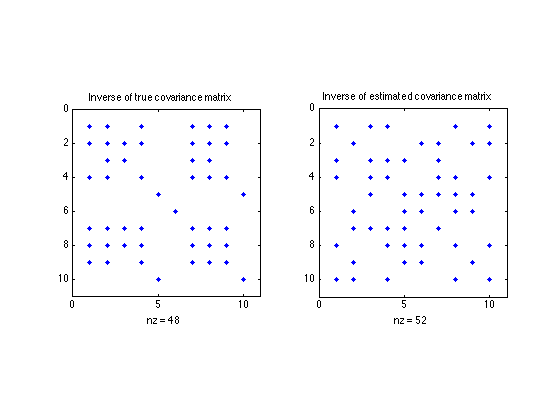

figure;

subplot(121);

spy(Strue);

title('Inverse of true covariance matrix')

subplot(122);

spy(S)

title('Inverse of estimated covariance matrix')

Successive approximation method to be employed.

SDPT3 will be called several times to refine the solution.

Original size: 503 variables, 280 equality constraints

1 exponentials add 8 variables, 5 equality constraints

-----------------------------------------------------------------

Cones | Errors |

Mov/Act | Centering Exp cone Poly cone | Status

--------+---------------------------------+---------

1/ 1 | 1.843e+00 3.337e-01 0.000e+00 | Solved

1/ 1 | 2.766e-01 6.363e-03 0.000e+00 | Solved

1/ 1 | 4.484e-03 1.630e-06 0.000e+00 | Solved

0/ 0 | 1.487e-05 0.000e+00 0.000e+00 | Solved

-----------------------------------------------------------------

Status: Solved

Optimal value (cvx_optval): -31.2401